Pushing the Pace in

a Resurgent Sri Lanka

a Resurgent Sri Lanka

The value created by the Bank for stakeholders through activities, relationships and linkages lead to the formation of capital external to the Bank.

They reside within our stakeholders, but the Bank has access to and makes use of these and its own internal capital in driving its business. Our discussion will now focus on the Bank's external capital formation, the material ones being, investor capital, customer capital, employee capital and social & environmental capital.

The Bank’s investors both institutional and individual, provide financial capital with the expectation of a return. The capital provided may be equity or debt, with the expected return typically covering a mix of short, medium and long term. These investors are of value to the Bank, and through the interaction of the various forms of financial and non-financial capital the Bank drives future earnings to derive value for itself and deliver value to its stakeholders.

As detailed under Investor Relations about 80% of the Bank’s share capital is held by institutions, which account for about 5% of our 8,014 shareholders. Residents, both institutional and individual, hold about 67% of the number of shares in issue, and account for 98% of all shareholders.

Satisfying this diverse mix of investors and their expectations is a strategic management responsibility that integrates finance, communications, marketing and compliance to create an effective two-way communication between the Bank, investors and other constituencies (see Stakeholder Engagement). Such engagement contributes towards our securities achieving fair valuation, which in turn helps investors to make informed buy or sell decisions, while providing market intelligence to the Bank’s corporate management. Our engagement includes other connected stakeholders such as analysts, media and regulatory authorities, as we believe that well-informed market participants are important for the functioning of an efficient capital market and the stability of the financial system as a whole.

The Bank's share price closed at LKR 250 on 31 December 2014, after trading at LKR 266 on 3 October 2014. The total market capitalization of the share largely improved during the year, and was ranked 16th on the Colombo Stock Exchange (2013: ranked 20th). More information is given under Investor Relations.

All shareholder return indicators soared during the year, indicating sound value generated for shareholders.

The Group Earnings per Share (EPS) for the year ended 31 December 2014 was LKR 25.14 with a 53% increase over the previous year, while Return on Equity (ROE) was 15.8%, up from 10.7% in 2013. Likewise, Total Shareholder Return (TSR) for the year ended 2014 was 63% (2013: 31%), which indicates the value created to shareholders through dividends and share price appreciation. The resultant Price Earning (PE) Ratio was 10 times as at 31 December 2014.

More details are given under Investor Relations.

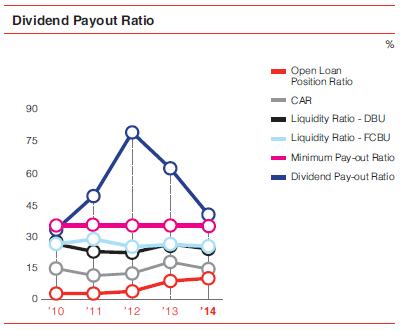

The Bank strives to provide shareholders with consistently high returns through profitable performance. The policy specifies that dividends gradually increase corresponding with growth in profits while taking account of inflation and future cash needs for sustainable operations. The latter requires striking a balance between a healthy payout with prudent ratios, as specified below:

| Ratio |

Policy guideline |

| Dividend payout ratio | >35% |

| Capital adequacy | >12% |

| Open loan position | <40% |

| Liquidity | >20% |

The Group's suite of core banking and capital markets products and services are delivered through the Bank and its subsidiaries respectively. They are designed with a customer focus and strong brand identity, and comprise of the following.

Innovation and new product development primarily take place through value addition to existing products, taking into account consumer needs and changing preferences. The Bank launched eight new retail banking products during the year under review, while several more were re-launched or modified for greater customer value and convenience.

The year commenced with the launch of NDB Salary Max, a new proposition exclusively designed for salaried individuals. The NDB Salary Max current and savings accounts are designed to help account holders to maximise the returns on their monthly salary, with account holders encouraged to open a savings account to inculcate a savings habit. While being a critical tool in developing the CASA accounts of the Bank, account holders have access to a fast track loan scheme against the net salary remitted to the Bank.

This is a concessionary loan scheme to encourage consumers to minimize their dependence on grid electricity by switching to solar power. With net metering regulations in place, this shift towards environmentally-friendly solar PV serves to reduce the demand for fossil fuel based energy from the national grid while providing cost savings to the consumer.

On the theme of supporting the education of young children, the Bank reformulated its approach to ‘Children’s Savings’ based on a focus group research carried out in 2013. The resulting NDB Shilpa minors’ savings account goes beyond enticing parents to deposit money and giving away freebies. Rather, the account is positioned to support the educational aspects and aspirations of account holders. It provides a measure of support to the child in the event the guardian is unable to fulfil the financial needs of the child while also rewarding the child for educational performance. Life insurance for the guardian is an important aspect, while the child gets education-related material as rewards for savings. Scholarships to top performing students are also an aspect of this product.

As a part of educating and sharing knowledge amongst children NDB Shilpa Peya programmes were conducted during the year in many parts of the country

Following a period of going slow for two years the Bank aggressively re-entered the home loans market in 2014 to make good use of the conducive market factors. Supported by the theme 'Freedom is having a home of your own', the product is targeted at salaried and self-employed individuals. The Bank also entered into strategic tie ups with reputed builders to complement this drive.

This new and unique product allows additional loans and overdrafts against the available collateral already held by the Bank for an existing Home Loan facility extended by the Bank. Thus, it does not require additional security, while being fast and hassle-free product for the customer.

Overseas travel was simplified with the introduction of NDB TravelPal travellers’ card, a prepaid Visa-accredited foreign currency card that enables customers to switch between up to 15 currencies loaded onto the card. This choice reduces exchange loss through multiple currency conversions and further reinforces the Bank’s commitment in providing value to customers.

The Bank rolled out a new suite of credit cards - dubbed ‘Good Life’ - available in five categories comprising Silver, Gold, Platinum, Signature and Infinite, during the year. Each type is designed with unique benefits and rewards to fulfil diverse lifestyle requirements of a wide range of customers. In parallel, a low interest ‘balance swap’ promotion was carried out to attract new customers who were weighed down by high interest rates on other credit cards.

The new suite of credit cards launched by the Bank during the year

NDB Educator is a tailor-made education loan designed to help aspiring youth to make their education and career dreams a reality. It is positioned as a convenient loan scheme where the student pays only the interest at a low rate during the study period, and repays the loan capital once the study course is completed. The product was launched during the year through many accredited Sri Lankan universities.

Alive to market trends in Sri Lanka, the Bank ventured into Islamic banking in August 2014. Branded as ‘NDB Shareek’ as yet another new Commercial Banking product, initial offerings were current accounts, Mudarabah savings and term deposits, Murabahah financing for local purchase and imports, Diminishing Musharakah for working capital financing, housing, vehicle and project financing, and Ijarah (leasing) for vehicle and equipment finance. Islamic banking is currently concentrated amongst corporate clients, but will expand to include SMEs through our branch network and relationship management teams of the Bank. We are fully equipped with a team that is both well trained and experienced in the area of Islamic banking. All Islamic banking operations are in accordance with the Central Bank of Sri Lanka guidelines and in conformity with Shariah principles, duly guided by a well-respected team of Shariah scholars.

Catering to high net worth clients, key initiatives during the year included sponsorship of the NDB Interschool Golf Tournament and a show featuring the best of West End and Broadway by the world-famous Tocata Musical Productions (UK) for Privilege members.

A participant at the NDB Interschool Golf Tournament held at the Royal Colombo Golf Club

The Ithuru Karana Maga savings drive was re-launched in October 2014 with a new look and feel across the country. The handy savings booklet that carries numerous tips and advice to inculcate the savings habit while improving one’s quality of life proved to be popular across varied segments of the population.

The Bank and its subsidiaries continually look for opportunities to bundle stand alone banking products and services offered by investment banking, wealth management and insurance with those coming from core banking, including micro and SME financing. Such bundling ensures a seamless integration of the wide range of financial solutions offered by the Group and provides a one-stop shop experience to customers.

Forming the backbone of Sri Lanka’s economy and as the principal source of employment creation, the Micro and Small and Medium Enterprises (MSME) sector has been an integral component of the Bank’s business since its founding. It has been a role that goes beyond the mere provision of financing.

The Bank's Micro Finance Strategy adopts two approaches in targeting underserved communities of the economy, namely, empowerment and capacity building (through the ‘Jeevana’ or ‘Life’ programme), and livelihood development financing (through the ‘Divi Aruna’ or ‘Awakening of Lives’ programme). Both programmes inculcate a business orientation that instils a strong credit culture, devoid of a ‘dole out’ mindset that is often associated with such initiatives.

A special feature of the Awakening Lives loan scheme is that facilities are granted without the need for collateral. Loan approval is based on the Bank’s assessment of the applicant’s capabilities and success of the enterprise, coupled with safety nets such as regular savings and insurance which are often new concepts to grass root level entrepreneurs.

Cinnamon has long held a significant position in Sri Lankan culture and economy, its earliest mention going back over two thousand years. Despite cinnamon’s potential to take on the world as a major export crop, its supply chain had not received the financial backing required to elevate the industry to the next level. The Bank ventured into this space in January 2014 through a national initiative that aims to empower the cinnamon industry in the country.

Through the ‘Awakening Lives’ programme of the Bank’s micro finance arm, we serve even the most remote village in any of the five cinnamon-growing districts of the country, encompassing the total supply chain from home garden cinnamon growers and tappers to product processors and exporters.

Loans - mainly for land preparation for cultivation and working capital - are tailor made for the cinnamon industry, ensuring that even the poorest will qualify for financial assistance. Coupled with building a strong credit culture among the beneficiaries, the Bank's role includes provision of technical knowledge and extension services, often in collaboration with government institutions. The latter include Ministry of Minor Export Crop Promotion, Department of Export Agriculture and regional Cinnamon Research Institutions.

Our venture into this sector also saw the opening of the Bank's 80th branch at Uragasmanhandiya, a bustling centre of action for cinnamon. Going forward, the Bank intends to team up with appropriate corporates to scale up access to global markets and ensure a viable, sustainable industry that takes Sri Lankan cinnamon to the world.

The Bank takes pride in suppor ting the efforts of cinnamon growers, processors and exporters as a part of its ‘Cinnamon to the World’ project

A pilot project under the Bank’s ‘Awakening-Lives’ programme was launched during the year targeting street food vendors at Colombo’s Galle Face Green. Strikingly, the loans have recorded 100% on-time repayments, with vendors also maintaining healthy cash build-ups on their savings accounts. Going the extra mile, the Bank has tied up with the Public Health Unit of the Colombo Municipal Council to conduct workshops and awareness campaigns on good hygienic practices relating to food handling.

Promoting self sufficiency at grass root level, the Bank spearheaded the financing of seed paddy farmers in Polonnaruwa in 2014. This initiative saw resurgence with Farmer Federations in the area repaying loans ahead of maturity, and paving the way for individual farmers to obtain financial facilities on their own accord.

Several tie ups were made with corporate and high-end SMEs to finance their grass root level suppliers, particularly small scale tea plantations and suppliers of liquid milk. Yet another success story was the financing of rural women in Gampola, who were the contracted suppliers of a large-scale soft toy manufacturer to international markets. Likewise, the Bank financed several small scale floriculturists in the Gampaha District and established partnerships between growers and exporters with the collaboration of the Sri Lanka Export Development Board.

The Bank conducted several financial literacy programmes for garment factory workers in Kilinochchi and Polonnaruwa, educating them on the basics of financial management, personal budgeting, investment options and savings.

As testimony to the Bank’s commitments for true financial inclusion the Bank was recognized as the sole global awardee at the Banker Magazine Awards - Financial Inclusion 2014

The Bank’s SME portfolio is well balanced across a wide range of sectors, as depicted under Financial Capital. SME financing during the year receive special emphasis on project financing (typically infrastructure as well as tourism, agriculture, transportation and health care sectors).

As discussed previously the Bank plays a key role in providing concessionary loans to the SME sector, both directly through its network as well as indirectly in its capacity as an apex bank for participating financial institutions.

Our SME product range includes trade financing services, channel financing, overdrafts, packing credit, bills discounting in addition to the traditional long term financing. A specialized product that stands out is the NDB trademark product suite that targets the tea manufacturing sector under the Tea Manufacturing Finance Programme. This gathered momentum during the year under review with several awareness creation programmes that were conducted by the Bank in several tea growing townships.

Asia Pacific Entrepreneurship Awards (APEA) is a regional recognition programme for outstanding entrepreneurs across Asia. The purpose of this Award programme is to cultivate a culture of honest, fair and responsible entrepreneurship across Asia. Enterprise Asia, a non-governmental organization for entrepreneurship based in Malaysia, is the owner and organizer of the APEA. Enterprise Asia, in association with Sri Lanka Malaysia Business Council (SLMBC) of the Ceylon Chamber of Commerce organized this event in Sri Lanka in 2012 and 2013, with great success. The Bank partnered with Enterprise Asia and SLMBC as the principal sponsor of both events signifying our commitment for building an entrepreneurial culture in Sri Lanka.

The Bank was the principal sponsor at the APEA A wards, signifying its commitment for building an entrepreneurial culture in Sri Lanka

Over 70% of the Bank’s SME portfolio is concentrated in the Western, Southern and North Western Provinces, largely reflecting population density, access to markets and business opportunity. However, things are changing fast with the massive infrastructure development taking place in the country. The Bank is alive to such changes and is proactively reaching out to support SMEs in other provinces through branch expansion and other means.

The Bank regularly engages with the SME community through workshops and seminars across the country, often supported by academic staff and industry experts. During the year 2014 such events were conducted in 8 administrative districts of the country. They attracted a total of 1,136 local participants who benefited from knowledge transfer, exposure to best practices and new insights.

The year 2014 saw the establishment of the first ‘customer loyalty group’, located in Kaduruwela - Polonnaruwa, with the active enrolment of over 150 small and micro entrepreneurs. Under the auspices of the Polonnaruwa Divisional Secretariat and the North Central Regional Office of the Central Bank of Sri Lanka, the Bank initiated a strong and loyal customer base as the initial step towards supporting income generating and livelihood development activities of grass root level entrepreneurs. It was an initiative which was much appreciated by the local community.

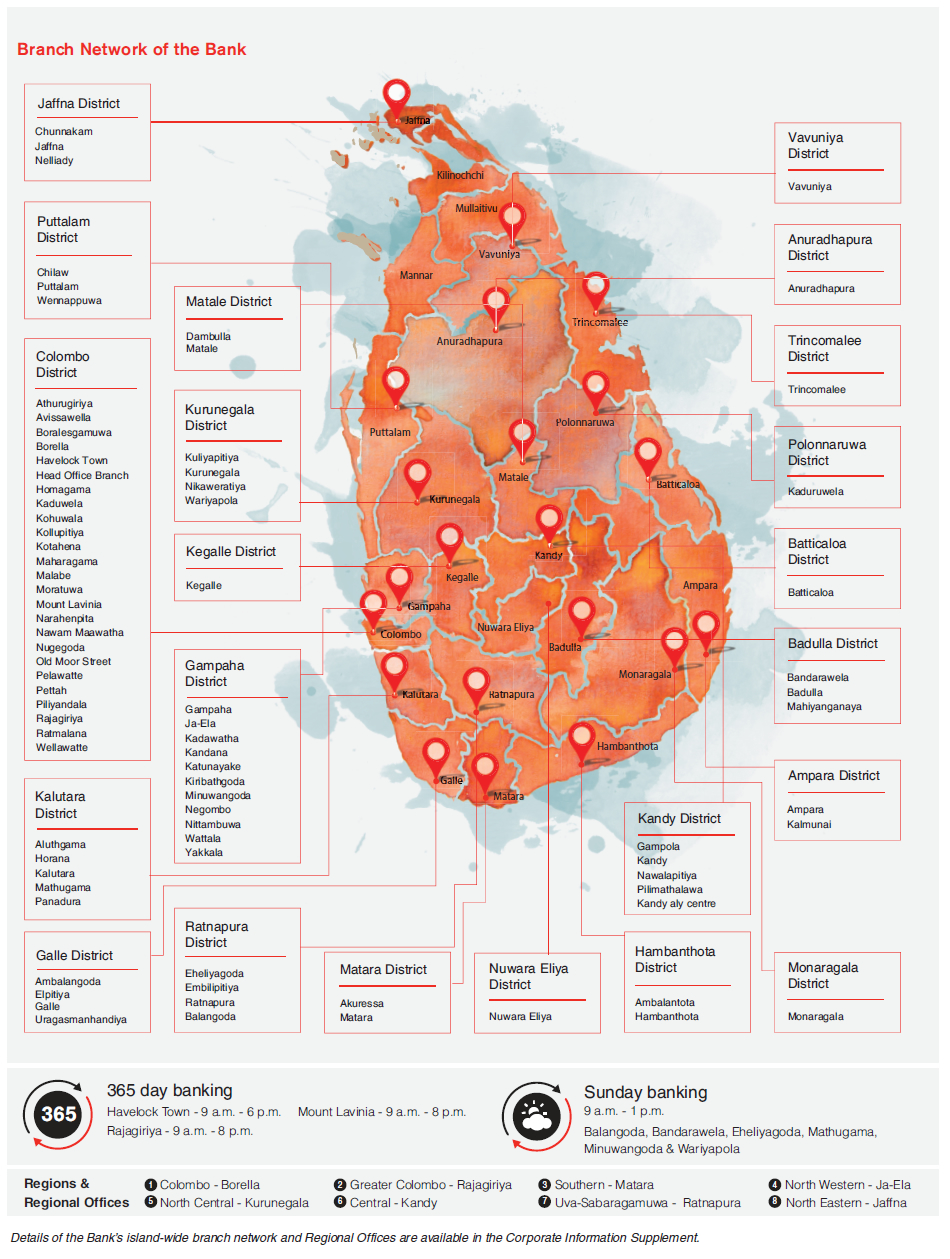

Our delivery channels include 83 branches, all LANKAPAY enabled ATMs around the country and VISA enabled ATMs around the globe. In addition customers have access through the Internet, mobile phones and card-based systems.

The Bank opened new branches in Balangoda, Uragasmanhandiya, Kandy City Centre, Old Moor Street - Colombo and Katunayake, thus expanding the network from 78 to 83 during the year. Our entry into Uragasmanhandiya is noteworthy, as this complemented our ‘Cinnamon to the World’ initiative by establishing a presence at the heart of the cinnamon growing area of the country. In addition to the five new branches opened during the year, five branches located in Negombo, Boralesgamuwa, Ratmalana, Athurugiriya and Narahenpita were relocated to more spacious premises, with emphasis on customer convenience. Of these five, four were extension offices which were upgraded to full service branches to cater to rising customer demand from the localities.

A gift being presented by the Branch Manager to a minor account holder at the Katunayake branch opening

Eight Regional Centres were established in 2013 to support the Bank’s growth. They continue to provide oversight over duly assigned branch clusters while ensuring the same excellence in service that customers associate with the NDB brand.

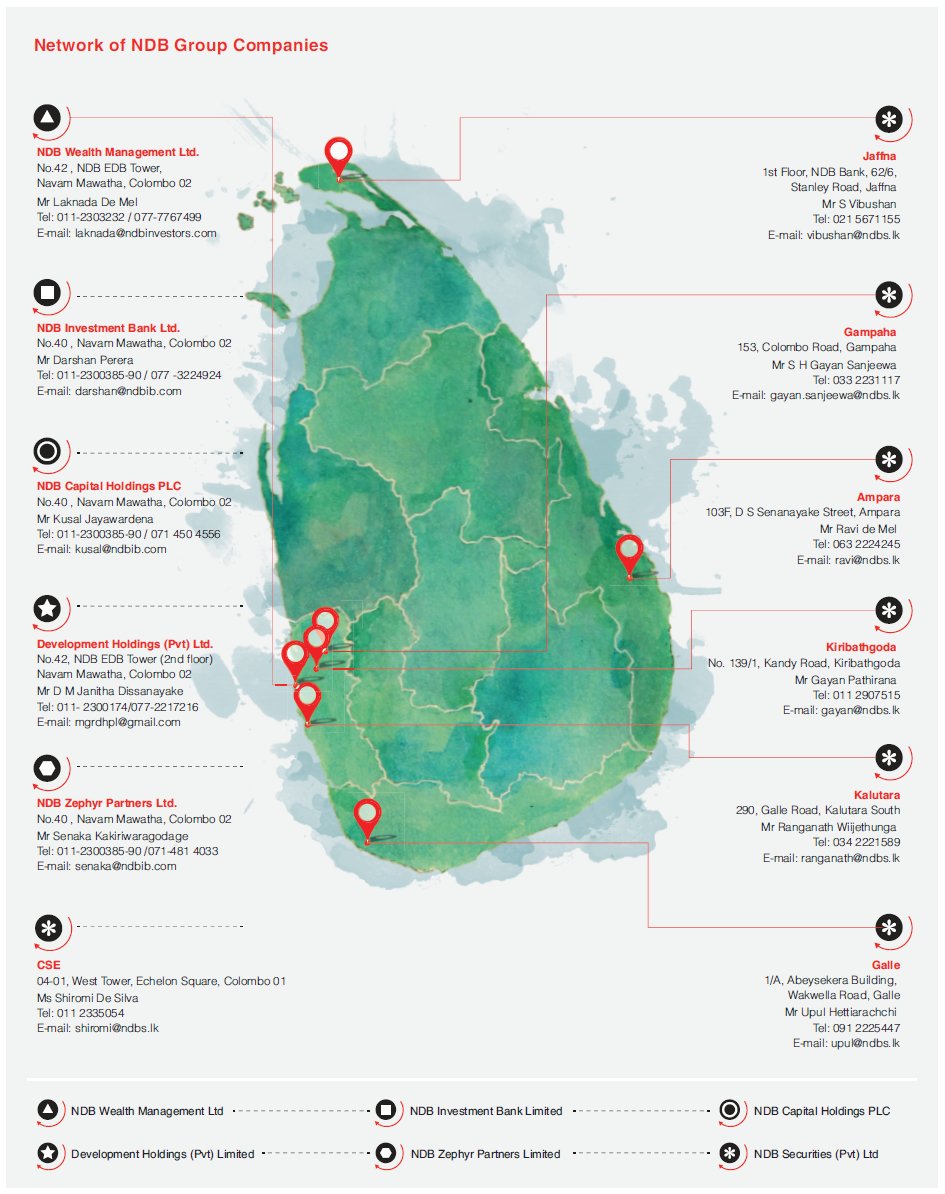

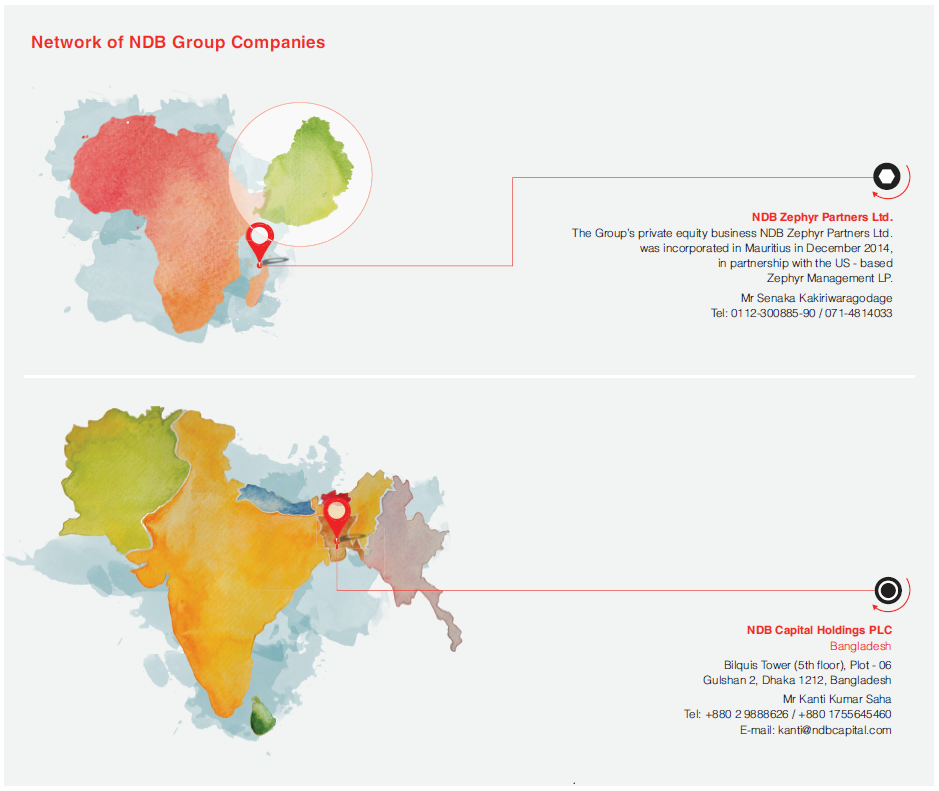

NDB Group partnered with Zephyr Management LP, a New York based global emerging markets investment firm, to set up the Emerald Sri Lanka Fund, Sri Lanka’s largest country dedicated private equity fund

Our first digitized branch was set up at the Kandy City Centre during the year. Aptly known as NDB Connect, it is equipped with modern digital touch screens and self-banking features that make day-to-day banking much more convenient. At NDB Connect customers have instant access to a wide array of information not only confined to banking products but also on savings and investment tools, house purchase and construction, vehicle purchase, education as well as entertainment features to engage children who visit the branch. The content is hosted in Sinhala, Tamil and English to cater to our diverse clientele.

A customer using the digital information portals at NDB's first digitized branch at the Kandy City Centre

In line with a national initiative, the Bank established connectivity with the Lanka Clear Common Payment Switch during the year. This common platform greatly increased the number of ATMs that our customers may use countrywide, from 74 in 2013 to 83 by end 2014.

This service is tailored towards the busy customer. The Bank agent visits the customer and provides basic banking services during normal working hours. The project is under testing and is expected to be fully launched in 2015.

As a part of our efforts to make the NDB brand more relevant in emerging market segments, the Bank continued to strengthen its online presence through its corporate website and social media engagement.

Making our entry into the social media platform with the launch of the NDB Facebook fan page in February 2013 (www.facebook.com/ndbbankplc), we ended 2014 with over 100,000 fans. Encouragingly, the Bank received two awards of excellence for the 'Best use of Facebook' and the 'Best use of Social Networks' at the 5th CMO Asia Awards for Excellence in Branding and Marketing held in Singapore. The awards recognized the great strides made by the Bank in the social and digital media marketing space in the banking industry within a short period of less than two years.

The NDB Facebook fan page provides the Bank with an opportunity to engage with a growing online community, while building brand awareness amidst a predominantly youthful audience. It is now the second-most viewed Facebook fan page in the Sri Lankan financial services industry; with an average of over 20,000 engagements per month and an average PTA (People Talking About) over 10,000, which is a phenomenal achievement for a FB page in the financial services industry.

The Bank also maintains individual product pages on Facebook to share relevant content with each type of audience the products are targeted at. NDB Salary Max Facebook page, published in January 2014, focuses on educating young executives on making the most of the salary they draw. ‘Cinnamon to the World’, also published in January, is a venture to promote Sri Lanka’s cinnamon industry. The page discusses the virtues, health benefits, historical details and vendor details of cinnamon while sharing cinnamon inspired food recipes in a venture to create awareness about the home grown cinnamon and its uses amongst local and global communities. The third individual page, published in March 2014, is NDB Shilpa. It is a page aimed at educating parents, parents-to-be and young adults on the saving habits for children and general tips on upbringing children.

Since the launch of the Facebook page the Bank has continuously strengthened its position across many other popular social media platforms including Twitter, LinkedIn, Youtube and Pinterest; sharing educative and stimulating content. The social and digital media presence of the Bank complements our communications strategy which also includes mass media, ground promotions and regional capacity building programmes.

The Bank conducted annual customer satisfaction surveys through Lanka Market Research Bureau (LMRB) in the past, the ratings received being 69.76% (2008), 75.40% (2009) and 75.43% (2010). This was replaced by a comprehensive research programme executed in 2012/13, also through LMRB. The mystery shopper results of the survey revealed that branch ambience was friendly and inviting with neatly displayed material and helpful staff.

Market research is carried out from time with particular focus on products, services, brand equity and the like, and the results are used for corrective action as well as seizing opportunities. For example, product insights received through a focus group discussion with customers of Children’s Savings Deposit product in 2013 resulted in changes and a re-launch in 2014 under the name NDB Shilpa.

A Call Out Programme was implemented in 2014 to gauge customer perception on the service levels maintained at the time of being newly introduced to the Bank. Customers to be contacted were picked from Bank’s core banking system and a sample 354 customers were contacted for the first phase of the survey.

Key findings indicated that 74% of the customers gave a rating of 8 and above (out of 10) to the officer who served them while 79% mentioned that they are very likely to recommend the Bank to others. The feedback received from the survey was shared with the relevant branches and front line service units for future action.

A dedicated customer service officer monitors service delivery and identifies gaps across all touch points of the Bank. Recommendations for service recovery and their implementation are monitored from end to end.

The Bank maintains a comprehensive online complaint management system where the complaints are resolved within a stipulated frame of time based on the nature and complexity of the complaint. Customers may also contact the Bank via email (contact@ndbbank.com which is also displayed on the website) with feedback, queries or suggestions.

Routine call outs are made to new customers who open new accounts or obtain loans from the Bank to assess the level of satisfaction at the point of delivery. Such feedback received is fed in to the relevant system (complaints/suggestions) and escalated to the customer service officer as well as the business heads in order to take corrective action, if any.

Continuous improvement is introduced based on the feedback received in customer surveys and ongoing customer feedback on the products and services. Several cross functional teams have been appointed from within the Group to identify strategic initiatives for value creation, product innovations and synergizing the Group in building the NDB Brand. These teams play a pivotal role in triggering the overall Group strategy through the implementation of key initiatives across customer segments with customised products and channels while leveraging the Banks’ competitive strengths and market dynamics.

Internally, the Bank encourages continuous innovation through its automated, suggestion generating system named ‘IdeaXpress’. It is an IT tool which can be accessed by all employees in the Bank to share innovative ideas and customer insights. The Bank also maintains a complaint management system for resolving customer complaints and grievances.

In this technologically savvy, data-driven society, customers demand clear information and transparency before making a purchase. Furthermore, with the popularity of social media and other online sources there are several avenues for dissatisfied customers to air their grievances, or even take legal action if product information had been misleading. Accordingly, the Bank takes care in providing accurate and relevant information in a manner that can be understood by a layman. Details of products and services offered are easily accessible in the form of printed material as well as through the Bank’s website. Contact details of relevant staff handling the products and services are displayed for additional information, while one may also inquire through the Bank’s 24-hour customer service hotline where trained customer service personnel are on hand.

The Bank conforms to the requirements of the Customer Charter of the Central Bank of Sri Lanka. This includes labelling and the provision of sufficient information on products, services, rates, tariffs as well as clearly displaying terms and conditions governing such aspects. We have not identified, nor have we been notified, of any significant cases of non-compliance with such regulations or voluntary codes. Further, the Customer Charter is made available on the Bank’s corporate website for transparency and easy access to information on consumer rights.

The Bank adheres to the regulations stipulated on the Customer Charter of the Central Bank of Sri Lanka in addition to the general rules and regulations of the country that govern the advertising and communications industry as a whole.

The Bank’s communications policy is structured within these parameters, and duly approved by the Board of Directors. It governs the objectives, division of responsibilities and general guidelines for communicating with various target groups, and covers the following aspects:

The communications policy is reviewed and supervised annually by the Board Audit Committee of the Bank.

There were no reported incidents of non-compliance with regulations and voluntary codes concerning marketing communications, including advertising, promotion, and sponsorship during the year under review.

The Bank maintains a comprehensive online complaint management system where complaints are resolved within a stipulated time frame based on the nature and complexity of the complaint. Once a complaint is lodged, it is escalated to the relevant head of department where accountability lies for resolution.

The Bank adheres to a strict secrecy policy to which all staff members are bound through the Code of Conduct. Further, the information technology platform of the Bank is maintained in house under strict confidentiality and is duly secured against malicious spyware etc. There were no substantiated complaints regarding breaches of customer privacy or loss of customer data during the year.

At the heart of our success lie our people: all driven by one common vision to build a world-class Sri Lankan bank. In turn the Bank is one that serves all its employees equitably and transparently through clearly articulated corporate values that underscore our human resource development agenda. It’s all about how the Bank builds its employee capital by attracting the best of talent, nurturing and moulding their development and rewarding performance.

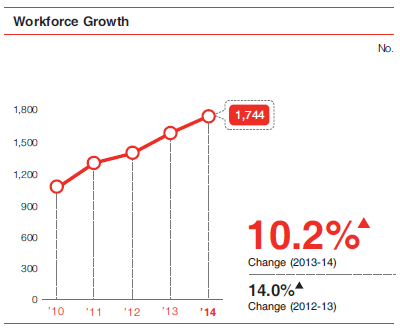

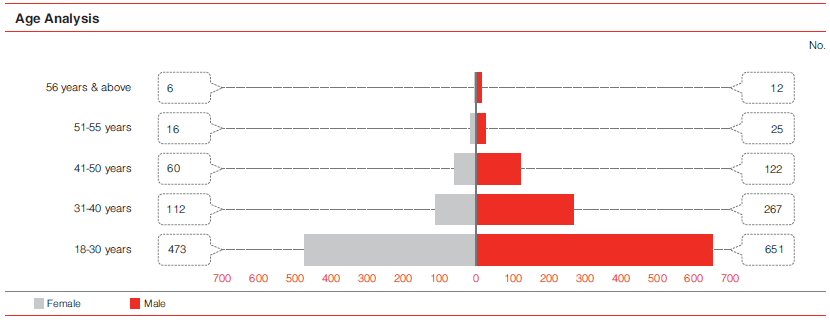

By end 2014, 1,744 people worked at the Bank, an increase of 10.17% over the previous year’s total of 1,583 persons. Women form well over one third of our workforce, including management grades; while the NDB Bank family is proud to say that it comprises people from diverse social backgrounds, ethnicities, religions and ages. The Bank draws on this diversity as inherent strengths to deliver big results.

| Number | Composition, % | |||||

| Grade | Female | Male | Total | Female | Male | |

| Senior management | 16 | 27 | 43 | 37 | 63 | |

| Management | 66 | 143 | 209 | 32 | 68 | |

| Executive | 77 | 194 | 271 | 28 | 72 | |

| Non-executive | 435 | 504 | 939 | 46 | 54 | |

| Specialized sales force | 25 | 177 | 202 | 12 | 88 | |

| Trainees and others | 48 | 32 | 80 | 60 | 40 | |

| Total | 667 | 1,077 | 1,744 | 38 | 62 | |

| Number | Composition, % | |||||

| Employment type | Female | Male | Total | Female | Male | |

| Permanent | 552 | 833 | 1,385 | 40 | 60 | |

| Contract | 49 | 48 | 97 | 51 | 49 | |

| Specialized sales force | 20 | 174 | 194 | 10 | 90 | |

| Trainee banking assistants | 42 | 17 | 59 | 71 | 29 | |

| Internships | 4 | 5 | 9 | 44 | 56 | |

| Total | 667 | 1,077 | 1,744 | 38 | 62 | |

Employees in the permanent cadre accounted for 79% of the total workforce by end 2014 (2013: 82%). In order to optimize business efficiencies, certain tasks are outsourced and critical aspects in respect of these tasks are carried out by contract cadre employees of the Bank. Contract cadre employees are also engaged for incentivized jobs such as the Specialized Sales Force.

| Number | Composition, % | |||||

| Location | Female | Male | Total | Female | Male | |

| Head Office - Colombo | 390 | 520 | 910 | 43 | 57 | |

| Region 1 - Colombo | 57 | 85 | 142 | 40 | 60 | |

| Region 2 - Greater Colombo | 47 | 67 | 114 | 41 | 59 | |

| Region 3 - Southern | 32 | 90 | 122 | 26 | 74 | |

| Region 4 - North Western | 44 | 90 | 134 | 33 | 67 | |

| Region 5 - North Central | 25 | 54 | 79 | 32 | 68 | |

| Region 6 - Central | 36 | 80 | 116 | 31 | 69 | |

| Region 7 - Uva-Sabaragamuwa | 16 | 46 | 62 | 26 | 74 | |

| Region 8 - North Eastern | 20 | 45 | 65 | 31 | 69 | |

| Total | 667 | 1,077 | 1,744 | 38 | 62 | |

Whilst fostering organic growth, duly supported by training, development and succession planning, the Bank also welcomes new thinking that comes with new blood.

A transparent procedure is in place for all staff recruitment, which is followed by induction and absorption. As an employer of choice, the Bank adopts some of the best industry practices in retaining staff. In addition to providing an attractive remuneration package, other aspects focused on retention include regular employee engagement, training and development, career progression, equal opportunity, parental leave, benchmarked compensation including share-based incentives and short-term variable bonus schemes.

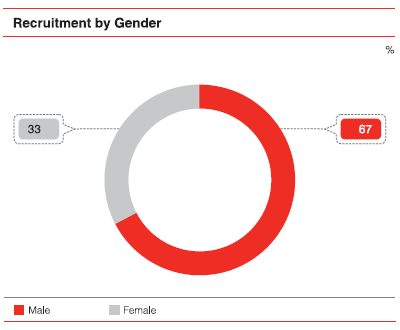

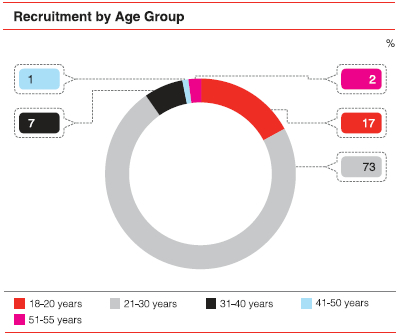

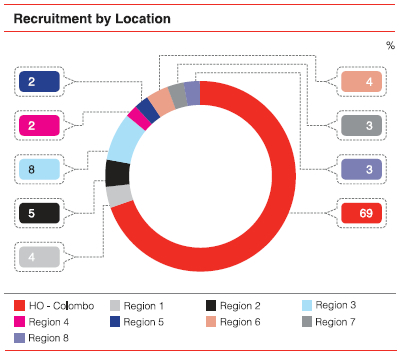

The Bank recruited a total of 379 persons during the year, with males (67%), the age group 21 to 30 years (73%) and those from Head Office (69%) accounting for the largest proportion of new entrants.

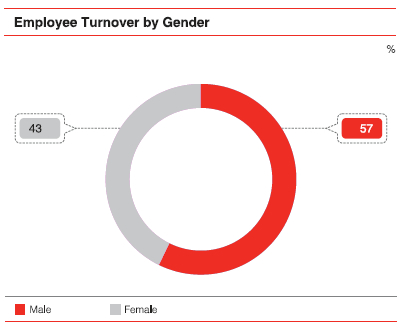

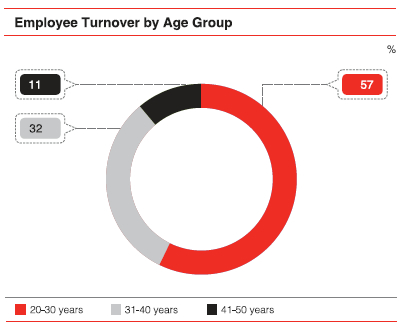

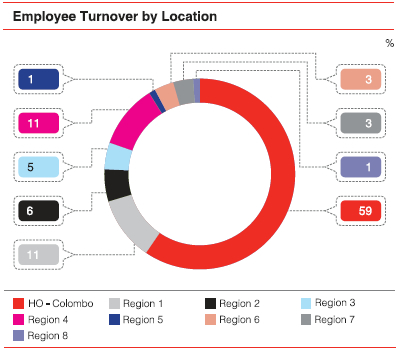

A total of 91 permanent employees resigned from the Bank during the year, with males (57%), the age group 20 to 30 years (57%) and those from Head Office (59%) accounting for the largest proportion of leavers.

The overall employee attrition rate during the year, measured as the percentage of employees leaving the Bank (excluding those retiring) amounted to 6.6% (2013: 4.9%). The Head Office had the highest number of resignations by virtue of the numbers employed.

Only female employees are entitled to parental (maternity) leave, and hence male employees are excluded in computing the return to work and retention rate statistics given below.

Return to work: Employees returning to work out of those due to return in 2014 - 73%

Retention rate: Employees who stayed on at least 12 months out of those due to return in 2013 - 23%

Employees of the Bank are entitled to a gratuity payment on resignation after having served a period of five years at the Bank. Whilst the Bank does not provide for a pension plan, a small proportion of employees who were employed by National Development Bank prior to the merger of 1 August 2005 remain eligible to a non-contributable private pension plan.

Employees are eligible for Employees’ Provident Fund (EPF) contributions (10% by employee, 15% by Bank), and Employees’ Trust Fund (ETF) contributions (3% by Bank) in accordance with the respective statutes and regulations.

Senior management staff may also participate in an Equity Linked Compensation Plan, subject to certain limits, terms and conditions.

Details of the above plans and professional actuarial valuations for Employee Benefit Liabilities are given in Note 40 to the Financial Statements.

The table below summarizes the benefits available to full-time employees, who may be either permanent employees or contract employees.

| Compensation | Permanent employees | Contract employees |

| Fixed compensation | Applicable | Applicable |

| Variable compensation | Applicable | Applicable |

| Long-term share based schemes | Applicable | Not Applicable |

| Other perquisites | Permanent employees | Contract employees |

| Subsidized loan benefits | Applicable | Not Applicable |

| Retirement benefits | Applicable | Applicable |

| Reimbursable expenses | Applicable | Not Applicable |

| Other benefits | Applicable | Applicable |

Employees are at the core of our business, and we invest in their continuous training and development. The programmes are geared towards identifying, developing and retaining talent whilst catering to the business needs and long-term goals of the Bank. Training needs are identified through staff performance reviews, assessment feedback and regular discussions with line managers. Training programmes are prioritized depending on operational urgencies and discussions with line management to identify and close competency gaps.

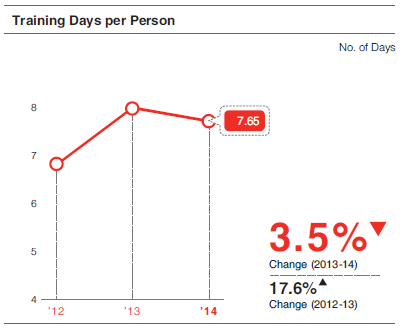

During the year, the Bank provided a total of 101,076 hours of training (2013: 95,695 hours) across all categories of staff.

Training is made available to staff based on needs and is independent of gender. The average duration of training per employee during 2014 was 7.65 person days overall, with 59.37 hours for females (2013: 65.72 hours) and 50.17 hours for males (2013: 55.86 hours).

| Designation | Band | Average of Hours | |||

| 2011 | 2012 | 2013 | 2014 | ||

|

Vice-President/Chief

Executive Officer/ Chief Financial Officer/Chief Operating Officer |

1 | 47.56 | 36.27 | 28.09 | 36.20 |

| Assistant Vice-President | 2 | 40.88 | 54.10 | 27.03 | 29.65 |

| Manager 1 | 3 | 25.60 | 48.88 | 26.50 | 17.86 |

| Manager 2 | 4 | 47.58 | 37.64 | 27.45 | 25.58 |

| Deputy Manager | 5 | 26.48 | 58.43 | 31.58 | 29.12 |

| Assistant Manager | 6 | 32.47 | 54.21 | 29.75 | 38.28 |

| Officer | 7 | 124.12 | 56.27 | 50.05 | 45.40 |

| Senior Associate | 8 | 34.72 | 58.42 | 53.12 | 49.89 |

| Associate 1 | 9 | 20.22 | 34.14 | 45.51 | 44.11 |

| Associate 2 | 10 | 14.95 | 24.35 | 38.69 | 36.24 |

| Assistant | 11 | 0.00 | 0 | 6.00 | 2.00 |

| Others | 0 | 83.14 | 85.31 | 172.90 | 133.99 |

Employees are encouraged to supplement externally provided training with self-learning and take control of their professional development. The Bank supports this through our investment in e-learning, which now has 30 modules.

In collaboration with the Institute of Bankers Sri Lanka and the Centre for Banking Studies we have continued to facilitate training programmes for staff. The former conducts in-house Certificate and Diploma programmes for employees, thus advancing their career prospects and contribution to the Bank.

As another facet of personal development, we initiated the NDB Toastmasters Club in 2013 and joined the Global Toastmasters fraternity. This has helped in unleashing the hidden potential of employees, not only in oral communications but also giving them confidence to participate in professional forums.

As part of our welfare initiatives, the Bank provides a range of training and assistance that supports lifelong learning and transition support. These programmes develop knowledge, competencies and learning that collectively benefit our employees.

As an equal opportunity employer we recognize that diversity in terms of ethnicity, gender, race, religion and age serve to strengthen the collective human talent of the Bank. While they serve to enrich our human capital, diversity arising from hiring locally helps the Bank to better align its business model to effectively meet the needs of local communities.

The Bank uses multiple channels - both personal and e-based - to engage with staff. Regular dialogue clears misconceptions, enhances transparency and builds trust. They also serve to inform, listen to opinions, ideas and grievances, and above all they underscore one's sense of belonging to the NDB family.

Christmas party organized by the NDB Staff Recreation Club for the children of employees of the Bank

The Bank takes pride in organizing a programme ‘Talent Within’, to recognize children of employees of the Bank who obtained all ‘A ’ grade results at their GCE O/L and A/L examinations

These are aimed at driving and supporting superior employee performance that complement the Bank’s seven pillars of business strategy.

The Bank conducts two Employee Satisfaction Climate Surveys each year. The ISO Employee Satisfaction Survey seeks to obtain information on the services provided by the Human Resources Department of the Bank and identifies ways in which processes may be strengthened in accordance with the four pillar strategy described above.

In the year 2013, the Bank undertook the Great Places to Work Survey which provided comprehensive information into the employee engagement levels of the Bank.

All employees are entitled to raise a grievance in relation to their employment at the Bank within 30 days of the occurrence of a given event. It may be raised through informal or formal channels. The latter would include weekly meetings held by the Leadership Team, Branch Managers meetings, Regional Manager Conferences and Quarterly Town Hall Meetings held for the executive cadre. It is also possible for a grievance to be directly referred to the CEO.

There were no material grievances from employees including grievances on human rights reported during the year.

Although the Bank does not have a formal collective bargaining process, it encourages an open door policy and has in place many mechanisms to encourage employees to discuss their grievances.

We reward employees based on performance with absolutely no bias based on gender or any other divisive factor. A new Performance Development System (PDS) with improved performance measurement metrics, objectivity and transparency was launched in 2013 and further refined during the year under review. To ensure buy-in and transparency the PDS was developed through a bottom up approach with feedback obtained from employees at various levels.

With long-term staff retention in mind, we reviewed and revamped the Bank's Equity Linked Compensation Plan in 2013, and have subsequently introduced a Special Merit Bonus Scheme to cover a larger number of employees.

Individual performance is assessed through a formal appraisal process against agreed objectives and targets, and is benchmarked against industry norms. All employees, irrespective of grade, are subject to this review process. The review process entails a mid-year review and a final review at the end of the performance cycle.

The remuneration mechanism at the Bank recognizes and rewards individuals according to their performance, irrespective of gender. Promotions and performance appraisal principles are free of gender bias and are applied to both male and female employees.

The ratio of the weighted average basic salary by gender, female:male for the Bank overall during the year was 0.9 :1. The corresponding ratios across grades were:

| F | M | |

| Senior management | 0.7: | 1 |

| Management | 1.1: | 1 |

| Executive | 1.1: | 1 |

| Non-executive | 0.9: | 1 |

| Specialized sales force | 1.2: | 1 |

| Trainees & other | 0.3: | 1 |

| Overall | 0.9: | 1 |

We believe in the dignity of every human being and respect individual rights as set forth in the UN Global Compact (UNGC) concerning human rights, labour, the environment and anti-corruption principles. The Bank adheres to these principles.

There were no incidents of any form of discrimination reported during the year.

Likewise, there were no incidents of child labour, forced and compulsory labour reported during the year.

The Bank recognizes the importance of providing a healthy work environment as well as the need to balance one's demands of work and family. Accordingly, Corporate Wellness Programmes are conducted from time to time while Corporate Fitness Centre facilities are offered to all employees. In addition, there are 44 trained first aid officers and 24 trained psychological first aid officers who are available at all times to assist staff while on duty.

During the year, three incidents related to occupational health and safety were reported (2013: 2) and duly addressed. The total number of days lost in relation to these incidents was 146 person days (2013: 101 person days).

Our approach to corporate social responsibility (CSR) is by design. As a responsible corporate citizen the Bank is ever mindful of the impact it makes on local communities and the environment, and its symbiotic relationship. It is a win-win approach that recognizes that the ability of the Bank to create value for itself over time is inextricably linked to the value it creates for others. Thus, our approach to CSR is aligned not only with the Bank’s values and strategic objectives but also with the expectations and needs of its stakeholders. It is an agenda that covers operational, strategic and philanthropic CSR initiatives. Monitoring of results is carried out directly by the Bank, with the involvement of staff at the head office and the branches, as well as our CSR project partners.

Operational CSR initiatives are based on the Bank's day-to-day business operations. They are not separately identifiable as such, as they are integral with normal business and serve to create value for the Bank as well as its multiple stakeholders over multiple time horizons. For brevity only material aspects that have identifiable impacts on local communities and the environment are discussed here.

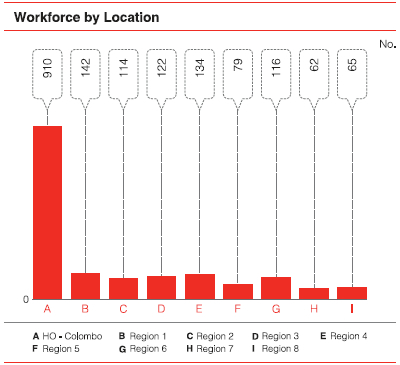

A broad geographical presence is important for business segments such as SME financing and retail fund mobilization. The benefits are mutual: local hires improve the diversity within the management team; they provide fresh insights on local needs that help us to tailor our products and services more effectively, while the local community too enhances its human capital. The Bank has consistently expanded its market position through organic growth in the past, and is represented in every province and 22 districts of the country.

| Employees in executive grade and above | |||

| Location by region | Total staff in the region | Total executive staff in the region | % From locality |

| Head Office - Colombo | 910 | 353 | 39 |

| Region 1 - Colombo | 142 | 31 | 22 |

| Region 2 - Greater Colombo | 114 | 24 | 21 |

| Region 3 - Southern | 122 | 19 | 16 |

| Region 4 - North Western | 134 | 29 | 22 |

| Region 5 - North Central | 79 | 19 | 24 |

| Region 6 - Central | 116 | 23 | 20 |

| Region 7 - Uva-Sabaragamuwa | 62 | 15 | 24 |

| Region 8 - North Eastern | 65 | 10 | 15 |

| Overall | 1,744 | 523 | 30 |

When placing employees in regions, priority is given to the hometown of each employee.

The Bank, since its founding, has been active in the development of the Micro and Small & Medium Enterprises (MSME) sector, a role that encompasses the provision of finance and much more.

Our approach to micro financing has two goals: (i) target underserved communities of the economy through empowerment and capacity building (the ‘Jeevana’ or ‘Life’ programme), and (ii) promote livelihood development through financing (the ‘Divi Aruna’ or ‘Awakening of Lives’ programme). Both programmes inculcate a business orientation that instills a strong credit culture, weaning the beneficiaries away from a dependency mindset.

The establishment of five dedicated SME Centres in the provinces, equipped with state-of-the-art facilities to support entrepreneurs bears further testimony to the Bank’s commitment to this sector. The Centres provide access to a wide array of information and online training modules, while also organizing seminars and workshops targeting the rural entrepreneur.

An account of the financial and non-financial impacts of our MSME development work is given under Financial Capital and Customer Capital respectively.

In addition to direct value creation and distribution through our own operations, the Bank’s investments and market presence impact on the local communities in many ways. They include jobs created or supported in the supply chain, development of local skills and knowledge, attracting investment and so on. The Bank’s strategic planning and management of its economic performance thus support a sustainable business that also makes a positive impact on the society and environment in which it operates. In short, they encapsulate the dual aspects of sustainable value creation.

The Bank’s Environmental and Social Management System (ESMS) serves to identify environmental and social risks in the projects and companies the Bank finances; and to take action to avoid, or failing, to minimize or to compensate for adverse impacts on the environment, workers and affected communities.

Our ESMS is an internally approved document that is an integral part of the Credit Policy and Credit Evaluation Process of the Bank for long term lending. It is available to all executives of the Bank. The ESMS requires clients to fulfil all national regulations in relation to environmental and social aspects. These include community consultations and impact assessments, with the depth of study depending on the nature of the project. The Central Environmental Authority (as the national regulatory body for environmental aspects) reviews applicable projects prior to granting approval for implementation.

The ESMS thus also serves to inculcate sound management practices on environmental and social aspects in client companies.

The Bank maintains a list of activities that are excluded for funding. Compliance is monitored on several fronts. A five-member cross functional team is responsible for the day-to-day operations of ESMS. The team includes an Environmental & Social Coordinator and a Technical Champion, both having received training in these fields. In addition, relationship managers in relevant departments, who have been trained in the day-to-day operation of the ESMS, follow up on the client's environmental licences annually and visit project sites at least once in every two years for monitoring.

Resource savings are achieved through continuous process improvements. For instance, automated document workflows minimize paper usage while improving turnaround time. An example is the Bank’s automated credit approval system, which is an online process that does away with paper based approvals, disbursements, memos etc.

Similarly, employees are encouraged to use electronic communications, online approvals and other web-based applications as much as possible, while documents are printed only if hard copies are strictly necessary. Waste paper generated in day-to-day operations is sent to a recycler. Used toner cartridges from printers, mobile phones and batteries no longer required and similar items are sent to authorized collectors who are equipped to handle hazardous waste. Obsolete assets such as computers and furniture that are still in working condition are donated to deserving institutions, while those beyond use or repair are disposed of responsibly through authorized collectors.

This is our first attempt at measuring and reporting our greenhouse gas (GHG) emissions. It is based on the most recent version of WBCSD/WRI Greenhouse Gas Protocol Corporate Accounting and Reporting Standard (2004) and Calculation Tools (2014). The boundary is limited to the Bank, which is also consistent with most of the aspects discussed in the Annual Report. Our reporting of GHG emissions under Scope 3, which is optional, is limited to sources that are material and measurable.

| Scope | Source | GHG Emissions | |

| tCO2e | % | ||

| 1 | Combustion in stationary sources | 22.2 | 0.6 |

| 1 | Combustion in mobile sources | 233.3 | 6.4 |

| 1 | Fugitive emissions from air conditioning equipment | 99.9 | 2.8 |

| Subtotal, Scope 1 | 355.4 | 9.8 | |

| 2 | Purchased electricity (CEB) | 1,990.6 | 54.9 |

| Subtotal, Scopes 1 and 2 | 2,346.0 | 64.7 | |

| 3 | Combustion in stationary sources | 52.1 | 1.4 |

| 3 | Purchased electricity (CEB) | 1,181.2 | 32.6 |

| 3 | Employee air travel | 47.4 | 1.3 |

| Subtotal, Scope 3 | 1,280.7 | 35.3 | |

| Total, all Scopes | 3,626.7 | 100.0 | |

The Bank’s total carbon footprint amounted to 3,627 tonnes carbon dioxide equivalent (tCO2e), with Scopes 1 and 2 together accounting for 2,346 tCO2e or 65% of the total.

Purchased electricity was by far the largest source of GHG emissions, with 1,991 tCO2e coming from premises owned or controlled by the Bank together with another 1,181 tCO2e from premises rented by branches. Taken together, purchased electricity accounted for 88% of the total carbon footprint of the Bank. The high proportion of electricity in the GHG emissions mix is to be expected considering the nature of our business and reliance on air conditioning in the climatic conditions under which we operate.

When related to an activity level, our GHG emissions intensity in 2014 was 311 kg CO2e per LKR million of the Bank’s total operating income. Going forward, we will further refine measurement procedures, benchmark results and consider expanding the boundary to include local subsidiaries. These are positive steps that will not only make the Bank and the Group more environmentally responsible, but also lead to cost savings through effective and efficient use of resources.

The Bank in collaboration with an accredited recycler makes every effort to collect the waste paper generated in its day-to-day operations for recycling. The Bank carries out a waste reduction and recycling drive through which waste paper amounting to 21,639 kg was recycled during the year, resulting in an estimated reduction in GHG emissions of 21.6 tCO2e and saved:

368 trees

37,976 litres of oil

86,556 kWh of electricity

687,687 litres of water

65 cubic metres of land fill

Education, particularly competency in a global language; and likewise, screening programmes to improve health of the people, are both important factors that contribute to the nation's economic growth in the long term. While these are also well aligned with the Bank's own business focus and strategy, ‘education’ lies at the core for our strategic CSR initiatives.

| Project | English Communication Programme for secondary school teachers | ||

| Objective | Enhance the standard of English in Sri Lanka | ||

| Partner | British Council, Colombo | ||

| Sustainability |

|

||

| Project | Schools Environment Awareness Programme | ||

| Objective |

|

||

| Partner | Biodiversity & Elephant Conservation Trust | ||

| Sustainability |

|

||

| Project | Chronic Kidney Disease (CKD) Screening Programmes | ||

| Objective |

|

||

| Partner | Kidney Protection Foundation, Renal Unit, Teaching Hospital, Anuradhapura | ||

| Sustainability |

|

||

| Project | Schools Library Project | ||

| Objective |

|

||

| Partner | Asia Foundation | ||

| Sustainability | Upgraded over 200 school libraries in all provinces of the country (to date) by providing high quality English language books. The project was commenced in 2008 and continues to date. |

Chief Executive Officer Mr Rajendra Theagarajah addressing a forum of 179 English teachers from over 87 government schools around the country who were awarded the ‘English for Teaching’ qualification validated by the British Council.

Chronic Kidney Disease Screening Programme at Anuradhapura

Philanthropic CSR initiatives are based on the identified needs at national level. The Bank has selected ‘Cancer Aid’ and ‘Prevention of Child Abuse’ as two areas for support, with assistance channelled through two Trusts set up for this purpose. In addition, the Bank partnered with an innovative bio-fencing project during the year that aims to alleviate an ongoing human-elephant conflict in some parts of the country.

| Project | NDB Cancer Aid Trust Fund | ||

| Objective | Provide assistance through the Cancer Hospital, Maharagama to patients who are unable to afford vital therapeutic items. | ||

| Partner | Cancer Hospital, Maharagama | ||

| Sustainability | LKR 8 million worth of donations made from inception of the Trust in 2008 onwards to date consisting of essential therapeutic items for patients as well as surgical items for the hospital | ||

| Project | Prevention of Child Abuse Trust | ||

| Objective |

|

||

| Partner | Department of Probation and Child Care | ||

| Sustainability | To date the Trust has conducted over 90 awareness programmes benefiting over 7,500 parents, 1,900 students, and 585 principals. In addition special awareness programmes have been conducted for 1,126 trainee teachers in seven national colleges of education. Over the years the Trust has also conducted special programmes for probation officers and caregivers. | ||

| Project | Palmyra bio-fencing Project | ||

| Objective | Prevent wild elephants from entering areas of human habitat and causing destruction by planting palmyra palms as a barrier, while serving as a resource for palmyra based products in the long-term. | ||

| Partner | Janathakshan, Sri Lanka (an NGO) | ||

| Sustainability | This is a pilot project limited to 1 km of fencing. Funding for the balance 21 km will be considered based on the lessons learnt. |

Prevention of child abuse awareness programme conducted for the trainee teachers of Pasdunrata National College of Education.

In an initiative to alleviate the human-elephant conflict in Sri Lanka staff members of the Bank were joined by volunteers from the village, including school children in the Palmyrah-bio fencing project conducted in Palugolla village in Nikaweratiya Pradeshiya Sabha of the Kurunegala District