Pushing the Pace in

a Resurgent Sri Lanka

a Resurgent Sri Lanka

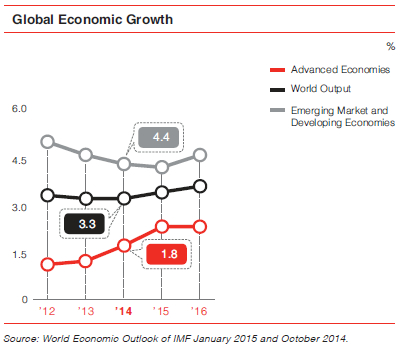

World output grew by 3.3% in 2014, on par with the growth in 2013. The key developments shaping the global economy during the year were:

| Year over Year | |||||

| Projections | |||||

|

(Percentage changes unless noted otherwise) |

2012 | 2013 | 2014 | 2015 | 2016 |

| World Output* | 3.4 | 3.3 | 3.3 | 3.5 | 3.7 |

| Advanced Economies | 1.2 | 1.3 | 1.8 | 2.4 | 2.4 |

| Emerging Market and Developing Economies** | 5.1 | 4.7 | 4.4 | 4.3 | 4.7 |

| Commodity Prices (U.S. dollars) | |||||

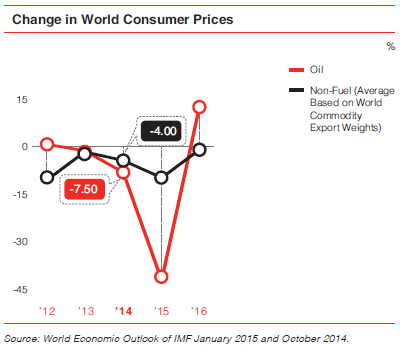

| Oil*** | 1.0 | (0.9) | (7.5) | (41.1) | 12.6 |

| Non-fuel (average based on world commodity export weights) | (10.0) | (1.2) | (4.0) | (9.3) | (0.7) |

| Consumer Prices | |||||

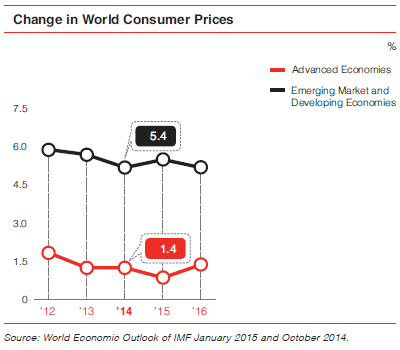

| Advanced Economies | 2.0 | 1.4 | 1.4 | 1.0 | 1.5 |

| Emerging Market and Developing Economies** | 6.1 | 5.9 | 5.4 | 5.7 | 5.4 |

| London Interbank Offered Rate (percent) | |||||

| On U.S. Dollar Deposits (six month) | 0.7 | 0.4 | 0.3 | 0.7 | 1.9 |

| On Euro Deposits (three month) | 0.6 | 0.2 | 0.2 | 0.0 | 0.1 |

| On Japanese Yen Deposits (six month) | 0.3 | 0.2 | 0.2 | 0.1 | 0.1 |

* The quarterly estimates and projections account for 90% of the world purchasing-power-parity weights.

** The quarterly estimates and projections account for approximately 80% of the emerging market and developing economies.

*** Simple average prices of UK, Brent, Dubai Fateh and West Texas intermediate crude oil.

Source: World Economic Outlook of IMF January 2015 and October 2014.

| Projections | ||||

| 2013 | 2014 | 2015 | 2016 | |

| Advanced Economies | 1.3 | 1.8 | 2.4 | 2.4 |

| United States | 2.2 | 2.4 | 3.6 | 3.3 |

| Euro Zone | (0.5) | 0.8 | 1.2 | 1.4 |

| Japan | 1.6 | 0.1 | 0.6 | 0.8 |

| Emerging Market and Developing Economies* | 4.7 | 4.4 | 4.3 | 4.7 |

| China | 7.8 | 7.4 | 6.8 | 6.3 |

* The quarterly estimates and projections account for approximately 80% of the emerging market and developing economies.

Source: World Economic Outlook of IMF January 2015.

Although global growth will receive a boost from lower oil prices, it is projected to be more than offset by negative factors, including investment weakness as adjustment to diminished expectations about medium-term growth continues in many advanced and emerging market economies.

Global growth in 2015 and 2016 are projected at 3.5% and 3.7% respectively following downward revisions in January 2015 by the IMF. The revisions reflect a reassessment of prospects in China, Russia, the Euro Zone and Japan as well as weaker activity in some major oil exporters because of the sharp drop in oil prices. The United States is the only major economy for which growth projections have been raised.

The Sri Lankan economy recorded a healthy growth of 7.8% (projected as at December 2014). Strengthening domestic economic activity and improving external demand contributed to the growth momentum.

The Agriculture sector grew only by 0.2% during the first quarter of 2014 due to adverse weather conditions, but the sector rebounded to record a growth of 6.4% in the second quarter, resulting in a growth of 3.1% in the first half of the year. The Industry sector grew by 12.4% with continued high performance in construction, mining and quarrying and manufacturing sub sectors; while the Services sector grew by 6.1% with improved performance in the wholesale and retail trade, transport and communication, and hotels and restaurants sub sectors.

* Extracts/sources: Central Bank of Sri Lanka - Recent economic developments: Highlights of 2014 and prospects for 2015, Department of Census & Statistics

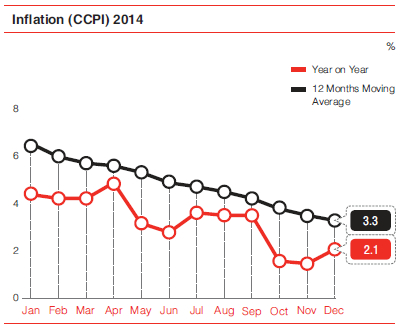

Year on year inflation measured by the Colombo Consumer Price Index (CCPI) remained below 5% during the year. Headline inflation (year-on-year) continued to record single digit levels, while core inflation remained equally subdued, indicating well contained demand driven inflationary pressures. Depicted below is the movement of the YoY inflation and the 12 months moving average inflation during the year as measured by the CCPI.

The BOP recorded a surplus of USD 1,954 million during the first half of 2014 as against a deficit of USD 169 million recorded during the corresponding period of 2013. Improved trade balance, other inflows to the current account and enhanced inflows to the financial account contributed to this significant improvement in the BOP.

The Sri Lankan rupee remained stable against the Dollar during the first nine months of the year, appreciating by 0.3%. Continued inflow of foreign exchange by way of current, capital and financial flows helped maintain the stability of the rupee during this period. Reflecting the cross currency exchange rate movements, the Sri Lankan rupee appreciated against the Japanese Yen by 4.5%, the Sterling Pound by 1.8% and the Euro by 9.1%, while depreciating against the Indian Rupee by 0.3% by end September 2014. The Central Bank intervention in the domestic foreign exchange market was mainly to absorb excess foreign exchange liquidity in order to prevent undue appreciation of the Sri Lankan rupee, particularly in the first eight months of the year. Accordingly, the Central Bank purchased USD 985 million from the domestic foreign exchange market on a net basis during the first nine months of 2014.

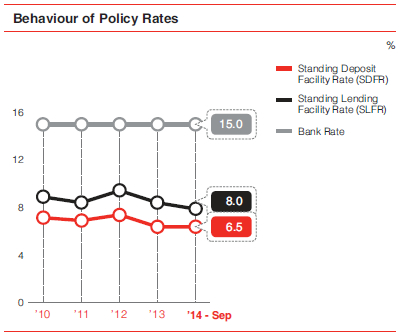

The monetary policy stance remained relatively eased during the first eight months of 2014 supported by benign inflation levels, which reflected well contained demand pressures as well as improved supply conditions. The Central Bank of Sri Lanka established a Standing Rate Corridor (SRC) in place of the policy rate corridor while introducing Standing Deposit Facility Rate (SDFR) and Standing Lending Facility Rate (SLFR) that replaced, respectively, the Repurchase rate and the Reverse Repurchase rate of the Central Bank.

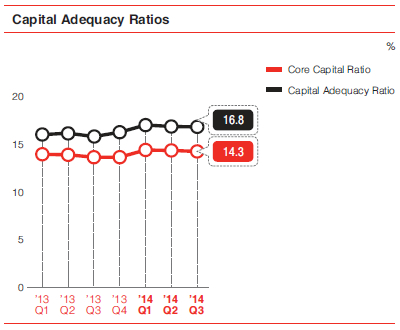

The financial sector expanded and remained stable during the period under review. The overall soundness of financial institutions improved with adequate capital and liquidity levels and an enhanced regulatory and risk management framework. The deceleration of credit growth however, impacted on the profitability of financial institutions. The financial sector consolidation process that was announced at the beginning of the year progressed well, and is expected to enhance the stability of the financial sector with strong and dynamic financial institutions.

The Sri Lankan economy is projected to grow at a rate of around 8% in 2015, with all sectors contributing to this growth. Inflation is expected to remain below 5% during the medium term. Sri Lanka’s external sector performance is expected to strengthen further in 2015, enhancing resilience to external shocks. The Sri Lankan economy is expected to move along a higher, non-inflationary growth path in the medium term, with the vastly improved physical infrastructure, improving social infrastructure, efforts to enhance overall productivity of the economy and the recovery of the global economy.

The Sri Lankan banking sector reached a total asset size of LKR 6,780 billion (as at November 2014), recording a 14% growth over the LKR 5,941 billion of December 2013. The growth trend was somewhat stagnant during the first nine months of the year, but escalated during the last quarter.

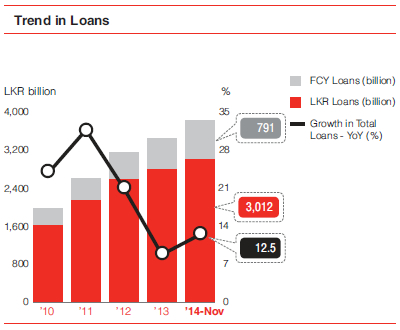

Total loans (LKR and FCY in total) reached LKR 3,803 billion as at end November 2014. Although the loan growth indicated a dip in early 2014 due to low credit appetite of the private sector, growth picked up during the second half of the year, recording a 11% growth for end November 2014, compared to December 2013.

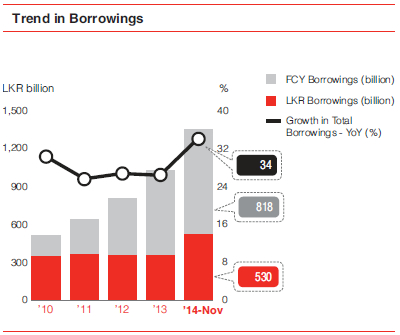

In terms of raising funds within the industry, there was greater focus in raising funds via rupee and foreign currency borrowings. Within total borrowings greater reliance was on foreign currency borrowings. By November 2014 the Sri Lankan banking sector had raised LKR 530 billion via rupee borrowings and LKR 818 billion via foreign currency borrowings.

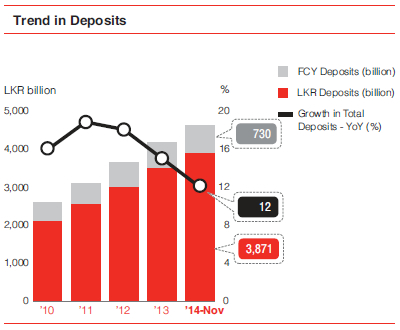

Deposits grew at moderate levels hovering around the 12% mark. The reduced interest rate environment that prevailed during the year made bank deposits less attractive to investors, causing a shift of funds from the banking and finance sector to capital market products and other asset classes. This is well reflected in the deposit growth rate of 10% as at November 2014 in comparison to December 2013.

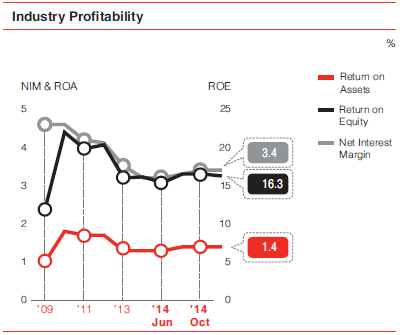

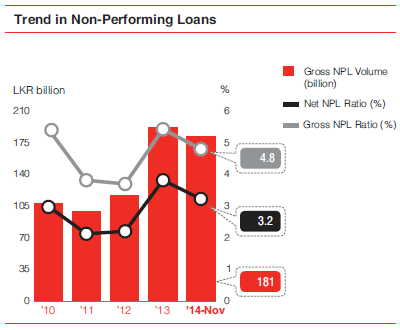

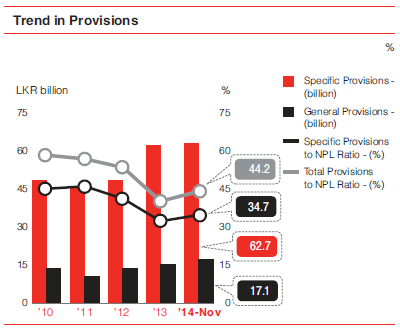

Profits during the first eleven months of 2014 improved compared to corresponding period of 2013 due to the lag effect in reducing interest rates on interest income compared to interest expenses, gains made on investments securities and lower level of provisions with improved NPL levels.

In 2013, the Central Bank of Sri Lanka, in its Road Map for the Banking & Financial Sector of Sri Lanka highlighted the need for at least five Sri Lankan banks with LKR 1 trillion or more assets by 2016. The need for such lager systemically important banks within the industry was triggered by the mammoth development projects that were being carried out in the country. The Road Map also brought to light the need for a large development focused bank which provides substantial impetus to development banking activities of the country.

Considering the development financing business embodied within the Bank and its counterpart DFCC Bank PLC, (together with DFCC Vardhana Bank PLC) the two entities were identified for the establishment of a significantly larger development focused commercial banking entity. In this context the two banks jointly engaged in a series of discussions during 2014, with Boston Consulting Group (India) Private Ltd. acting as consultants to advise the banks on the amalgamation process.

Thus far, there have been no definite decisions on any aspects of such consolidation and the final decision would be dependent on factors such as arrangements being agreed whilst safeguarding the interest of the investors, customers, employees and other stakeholders of the banks. Moreover the consolidation of the banks will be dependent on regulatory approvals and the passage of facilitative legislation.